North Dakota State Univ. recently published information about the effect of International Emergency Economic Powers Act tariffs on fertilizer prices and demand, and the "price stickiness" farmers are still feeling even though wholesale prices have seen relief.

Below is a summary of NDSU's report on tariff issues and costs in the Agricultural Trade Monitor. You can also read the entire report here.

- IEEPA tariffs collected an estimated $958 million in revenue from selected agricultural input imports during February–October 2025. Of this total, about $273 million came from agricultural chemicals, $530 million from farm machinery, $110 million from fertilizers, and $44 million from seeds.

- Tariff revenue is relatively modest compared to overall production costs. Despite their negative effects on producers, the collected tariffs represent a relatively small share of production expenses. For fertilizers, less than 1% of annual U.S. expenditures are spent on this input.

- Fertilizer tariff exposure was partially limited by exemptions, trade adjustment, and seasonal timing. Fertilizers benefited from exemptions under trade agreements such as USMCA, while IEEPA tariffs on remaining fertilizer imports were in effect primarily during the low‐demand season. Importers front‐loaded purchases ahead of tariff implementation and shifted sourcing toward exempt countries like Russia. Despite this trade diversion, overall imports still declined significantly, particularly for DAP and MAP, as foreign exporters redirected supplies to other markets.

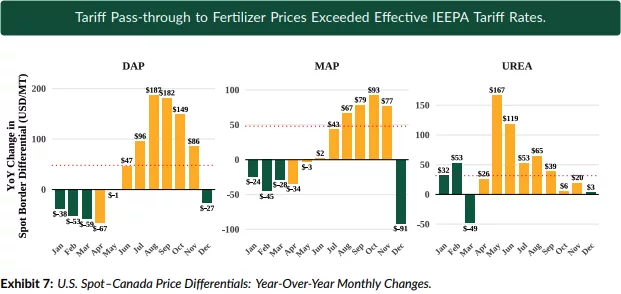

- Tariff pass‐through to farmer prices exceeded the tariff itself (more than complete pass‐through). During peak tariff months, fertilizer pass‐through exceeded the effective tariff rate. This excess pass‐through likely resulted from supply chain disruptions and uncertainties surrounding the tariff policy, meaning U.S. farmers and input suppliers may have borne economic costs substantially greater than the tariff revenue itself.

- November fertilizer tariff rollback brought price relief to wholesale markets. IEEPA tariffs raised DAP and MAP prices by more than $50/MT during parts of 2025. Following the tariff exemptions granted in November, U.S. price differentials with Canada caused by the tariffs converged back to normal. DAP spot prices have retraced most of their tariff‐driven increases, and MAP prices have fully reversed their increases, trading slightly below pre‐tariff parity.

- Retail fertilizer still carrying tariff effects. Wholesale prices fell sharply after the November rollback, but retail prices are adjusting more slowly. As of early January 2026, farmers buying fertilizer from local retailers continue to face price stickiness, paying tariff‐induced premiums above pre‐tariff baseline levels.

- Low Mississippi River levels in 2025 limited disruptions. Despite very low levels reached late last year, barge rates and grain movements were largely stable, with Mississippi basis spreads showing no severe market stress.

- China reaching soybean purchase commitments. Cumulative U.S. soybean sales to China total 8‐9 MMT. When transactions reported as unknown destinations are included, total sales reach approximately 13 MMT, exceeding the 12 MMT target. Despite U.S. soybeans trading at a significant price premium relative to Brazilian supplies, China has maintained its purchasing pace, suggesting strategic rather than price‐driven buying.